Simona Gotsova

Simona Gotsova

Public Finances

Interview | The biggest risk to the Bulgarian economy in 2026 is the crisis in the Middle East

Inflationary pressure driven by rising fuel prices will lead to more corporate bankruptcies and weaker domestic consumption

Mateusz Dadej, Coface Regional Economist for Central and Eastern Europe (CEE):

© ECONOMIC.BG / Coface

~ 5 min read

- Corporate insolvencies in Bulgaria are expected to start increasing in 2026;

- High prices are expected to weaken domestic demand;

- Higher inflation is beneficial for Bulgaria’s public finances;

- A tax increase is considered an unlikely scenario;

- The full benefits of adopting the euro will depend on whether Bulgaria implements the necessary reforms.

Economic.bg spoke with Dr. Mateusz Dadej, Head of Economic Research for Central and Eastern Europe (CEE) at Coface, where he monitors economic developments across the CEE region, inflationary trends, energy markets, and the impact of geopolitical crises on businesses and public finances.

In the interview, we discuss the state of Bulgaria’s public finances, trends in corporate insolvencies, the risks and benefits of euro adoption, as well as the consequences of the Middle East crisis for the Bulgarian economy.

Mr. Dadej, in its latest report, Coface stated that corporate insolvencies in Bulgaria declined in 2025. What are the main factors behind this trend? Have entrepreneurs adapted to the ongoing political uncertainty?

We have some preliminary data to believe that insolvencies decreased in Q1 but only based on bankruptcies numbers from Eurostat. I think it’s still early to say anything with sufficient degree of certainty what has happened in Q1.

But the trend for a few years is clear, the business insolvencies are in a downward trend. To some extent that is a normalization following particularly turbulent 2020-2022, when Insolvencies in Bulgaria did increase, peaking in 2022. The subsequent decline reflects both the normalization of the global environment and an improvement in Bulgaria’s domestic macroeconomic conditions.

Since 2022, energy prices have stabilized and Bulgaria’s economy has continued to expand. As a matter of fact, cumulative GDP growth since Q1 202 has reached roughly 11%, placing Bulgaria among the fastest‑growing economies in the region and across the EU. This suggests that the corporate sector has become more resilient to political uncertainty and has adapted to operating under such conditions. As political instability became persistent rather than episodic, firms and households appeared to have grown increasingly indifferent to the ongoing turbulence.

What are your expectations for the remainder of the year? Will insolvency cases continue to decrease, and what will be driving this development?

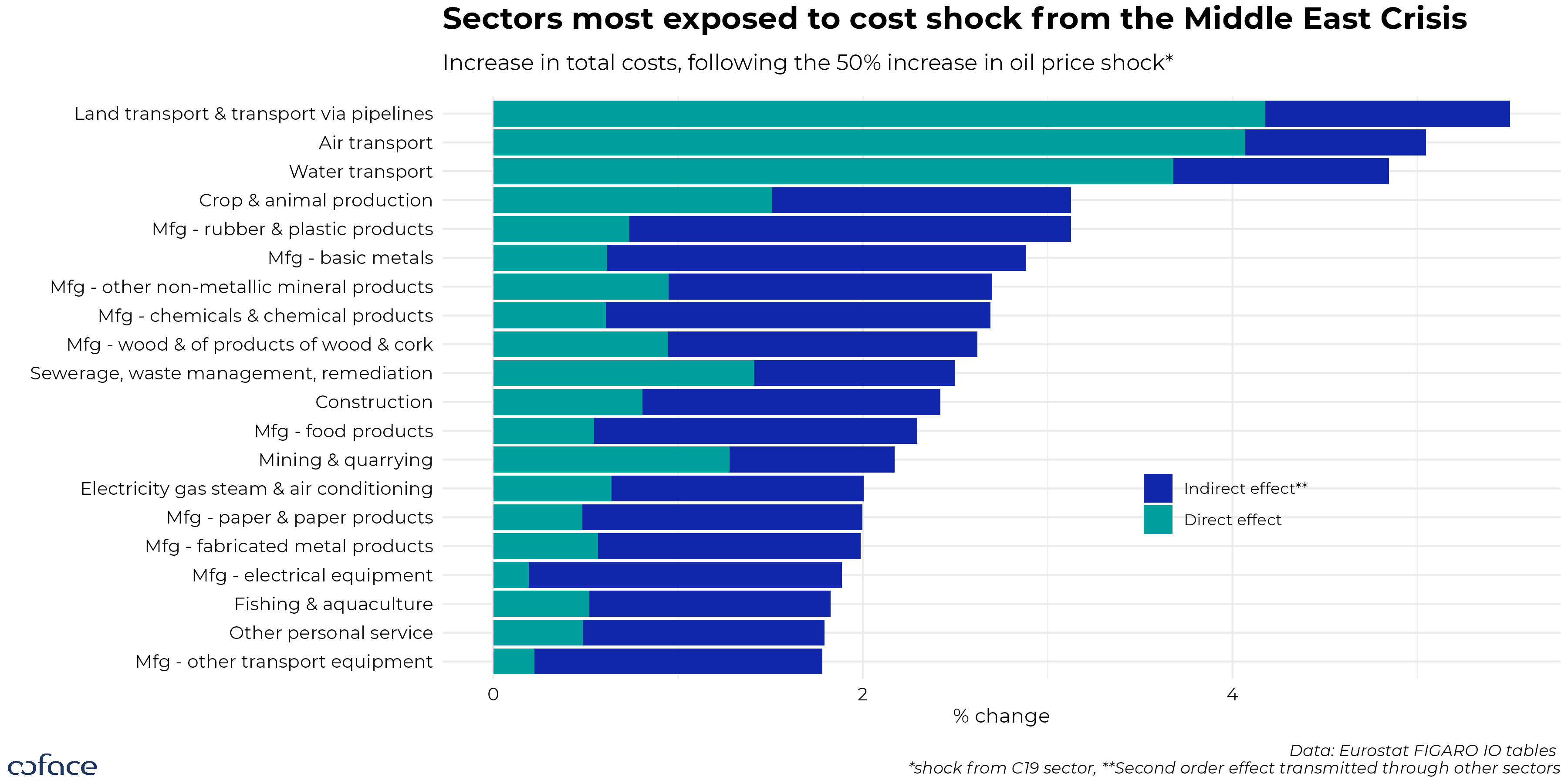

I believe we may have reached the end of this favorable trend. We expect business insolvencies in Bulgaria to increase this year. The firm sector is currently experiencing a massive and broad cost shock, which will compress their margins. The recent surge of inflation from 2.8% to 6.2% in April is just the beginning. The consequences of the Middle East crisis will not be limited to crude oil and natural gas, but also other commodities such as fertilizers, aluminum and petrochemicals. Because of the wide range of its usage, the shock will spillover to other goods, exacerbating the cost shock. According to our estimates, the sectors that will be the most affected, either directly (by increase in fuel affected commodity like crude oil) or indirectly (by exposure to other affected sectors) will be transport, agri-food and manufacturing – especially chemical sector.

Chart source: Coface

Moreover, Bulgarian households allocate a relatively high share of expenditure to fuel (around 5 per cent), implying a greater risk of demand reallocation away from domestically produced goods. Therefore, the firm sector in Bulgaria will operate in an environment of weaker domestic demand.

Coface has revised down its forecast for Bulgaria’s economic growthdue to the crisis in the Middle East. Is there a possibility of further downward revisions if the disruption of the Strait of Hormuz persists?

None knows how long the blockade of the Strait of Hormuz will last, but one thing is certain – with each day it last for one day too long. The longer the Strait of Hormuz is blocked the more severe consequences will be experienced globally, and Bulgaria will not be an exception. 20% loss of the global supply of crude oil can be offset in the short term by utilizing inventories. But there’s no way of balancing this supply loss without a significant reduction in economic activity, through demand destruction. This will become evident the closer we are to running out of global inventories.

Current GDP forecast of 2.4% is still up to date, but the risks are definitely skewed to the downside. Friday Q1 estimate of GDP may provide new information as well, but real consequences of the crisis will be evident from Q2 onward.

What are the biggest risks facing the Bulgarian economy this year?

The most important one is prolonged blockade of the Strait of Hormuz.

Could deteriorating public finances lead to higher taxes this year?

I don’t think this is likely scenario. The fiscal policy is indeed getting more expansionary, but it’s far from being excessive. Bulgaria maintains a strong economic growth and the incoming inflation will increase the nominal growth of economy; this should increase the nominal revenue. Higher inflation may not be good for the economy, but it sure is good for public finances.

But ultimately this is a matter of political will, and it does not seem like Rumen Radev is willing to increase taxes. Although he’s been rather vague on his economic agenda so far, he has been supportive of the recent national protests, which among other things were against the increase in taxes. Such turn from Radev immediately after forming the government would result in a let down of its electoral base.

What are the key positive factors that could support GDP growth? Is euro adoption among them?

Yes, Euro adoption in January 2026 is a major milestone and an opportunity for Bulgaria to strengthen institutions, enhance policy credibility, and raise medium-term growth. We expect that the adoption will lower sovereign risk premium, boost investor confidence, reduce currency risk and transaction costs, and loosen financial conditions. Some of these benefits are already visible in narrowing sovereign spreads and recent credit rating upgrades.

However, realizing the full growth potential of euro area accession will depend critically on relevant reforms and policy continuity amid the current political fragmentation. The reform that will be crucial include are related to governance, including improvements in state owned enterprises governance, anti-corruption measures, rule of law, judicial efficiency, procurement transparency, and energy-sector oversight. These reforms will reduce market distortions, build public trust, improve non-price competitiveness, and make Bulgaria a more attractive destination for investment, thereby embracing the long-term economic benefits of euro adoption.

In your report “Bulgaria 2026: A Promising Leap Towards the Euro”, you noted that a large share of the Bulgarian population opposes the euro, which could weaken the transition process and ultimately reduce its economic impact. Do you still see such risks, or has the outlook changed?

I believe the most challenging time in transition is behind us and from now on the benefits will be more pronounced. Potentially chaotic transition to Euro could have created a long-lasting negative sentiment in Bulgaria to the currency. But my judgment is that the transition turned out seamless and the effect on the broad inflation has been close to zero. What I consider a risk right now is a misattribution of the current increase in inflation to the euro adoption instead of the middle east conflict. This could indeed risk decreasing the support for Euro and integration into European Union.